What Does Property Owners Insurance Coverage Cover? A Full Overview You can also purchase riders to make sure you are covered versus certain risks or hazards that you would certainly not otherwise have coverage for. Damage because of the roof covering's age, basic damage, or overlook, however, will not be covered by your plan and you will need to spend for those fixings on your own. Whether you have a home or you're in the marketplace to acquire one, you already know exactly how crucial it is to protect it from the myriad of risks endangering to damage it. Ensuring that you have the ideal kinds and amounts of house owners insurance policy is among the most intelligent actions you can take as a property owner. Water damages to your home can be costly and time-consuming to repair. Here's what you need to find out about your insurance protection and exactly how to stop more damage.

Does Home Owners Insurance Policy Cover Wind Damage?

What type of water damages is not covered by house owners insurance coverage?

Flooding is the No. 1 natural catastrophe in the USA, yet house owners insurance does not cover this hazard. Generally, any type of water that flows right into your home from the ground isn't covered. So rain, a rising river and saturated ground aren't covered.

If rainfall slowly drips in through a leaking skylight and you try to sue for damage that developed over weeks or months, your insurance firm will likely hold you responsible for the damages. Bankrate.com is an independent, advertising-supported author and contrast solution. We are compensated for placement of sponsored product or services, or by you clicking on certain web links posted on our site. Therefore, this settlement may influence just how, where and in what order items show up within providing groups, other than where forbidden by legislation for our home mortgage, home equity and other home loaning items. Even if flooding isn't covered does not mean your house owners insurance coverage will not pay for any type of water damage. As a matter of fact, most conventional property owners Helpful hints insurance coverage include coverage for sure types of water damages-- as long as it's unexpected, unintended, and not the result of climbing floodwater. Your house owners insurance policy could cover water damages in your basement if it was brought on by something like a ruptured pipeline, however usually, house owners insurance policy does not cover flooding.

Ordinary Home Insurance Coverage Prices By Zip Code

See exactly how DSI can help give you or your organization the protection you need.This suggests damage from tornado surge, overflowing rivers, or a neighboring body of water is not covered.Water damages triggered by a ruptured pipeline will generally be covered by your property owners insurance plan, as long as the discharge was unexpected and unintended.

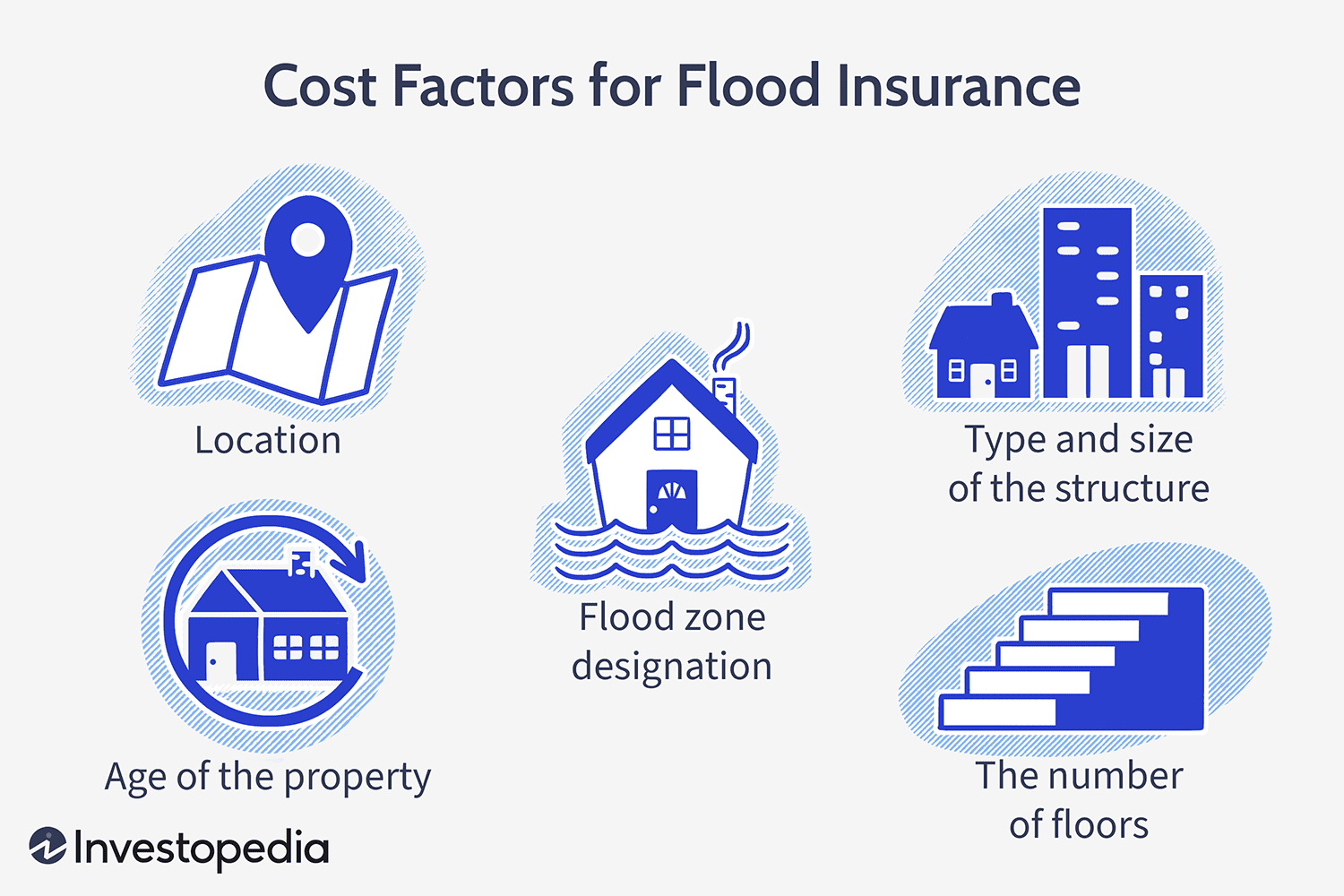

While these protections are necessary, it's essential to recognize that flood damage is a separate threat that requires specialized insurance coverage. Don't think your house owners insurance coverage will certainly secure you from the economic impact of a flood-- obtain a flooding insurance policy quote right here to safeguard the insurance coverage you need. If you have a flood insurance policy, the first step to take is to begin the claim procedure by suing with your insurance policy agent, broker or business. Tips for suing after a loss can be discovered on our main Calamity & Flooding Source Facility. The insurance company will send an insurer Visit this link out to evaluate the damages and examine whether they are covered by the policy. To shield your home versus floodings and storm surges, you ought to acquire a separate flood insurance plan, which you can usually purchase through the exact same firm that guarantees your home. That suggests if your basement floodings during a cyclone, you'll need a different flood insurance policy to cover the flood damage. Covering that danger indicates purchasing a separate flooding insurance coverage, either with the National Flooding Insurance Program (NFIP) or an exclusive carrier. HO-3 policies are one of the most typical property owners insurance coverage on the marketplace. Under the HO-3 policy type, personal property protection typically makes up 16 named dangers. Additional living expenses are restricted under most policies and just cover quantities beyond your typical living costs. Criterion property owners plans do cover some sorts of unexpected and accidental water damages and/or mold and mildew, consisting of burst pipelines, and sometimes sewage system back up or sump pump failure if you have that insurance coverage. Nonetheless, even if your policy covers these sorts of water damages, some business have begun to particularly omit or restrict coverage for mold that results. Failure to maintain flood insurance coverage-- for both occupants and home owners-- could result in the denial of future government calamity help. If the building is not in a high-risk area, but instead in a modest- to low-risk location, government law does not call for flood insurance, however, a lender can still require it. As a matter of fact, over 20 percent of all flooding insurance policy claims originated from locations beyond mapped risky flood zones.